Menu

Taxation for Growth in KP: A focus on Sales Tax on Services

With growing concerns regarding provincial revenue generation and complex center-province relations post-18th amendment, the issue of sales tax on services has emerged at the forefront of many discussions between the federation and its four provinces. While, the primary purpose of sales tax on services is to generate revenue for the provinces, there is a growing need to harmonize the sales tax regime in Pakistan, create a distinction between the taxing powers of the Federal Board of Revenue (FBR) and provincial revenue collecting authorities, and devise common rules and definitions for efficient data sharing.

Background

Pakistan inherited the tax structure of pre-partition India as per the Government of India Act and since then Services Sales Tax (SST) has remained a provincial subject – however, Goods Sales Tax (GST) was federalized in March, 1948. Although, this power to levy sales tax on services rests with the provinces, the FBR has been providing institutional support due to limited provincial capacity[1].

After the 7th NFC Award in 2010, provinces created their own revenue authorities and tax legislations. KP, for example, established the Khyber Pakhtunkhwa Revenue Authority (KPRA) in 2013 to administer and collect sales tax on services in accordance with the KP Finance Act, 2013. However, Value-added Tax (VAT) in Pakistan continues to have a fragmented base, as the sales tax on goods is administered by the federal government and the sales tax on services is collected by the provinces. This fragmentation has led to problems of clearly classifying transactions of goods and services, production inefficiencies, and compliance costs.

Khyber Pakhtunkhwa’s Experience

Provincial taxes play a key role in the overall growth agenda for KP and have had a significant impact on the recent budget, which reflects KP Government’s priorities regarding improving the performance of the sales tax on services. Currently, a total of 92 services are taxable under the Schedule 2 of Sales Tax on Services Act in Khyber Pakhtunkhwa (KP).

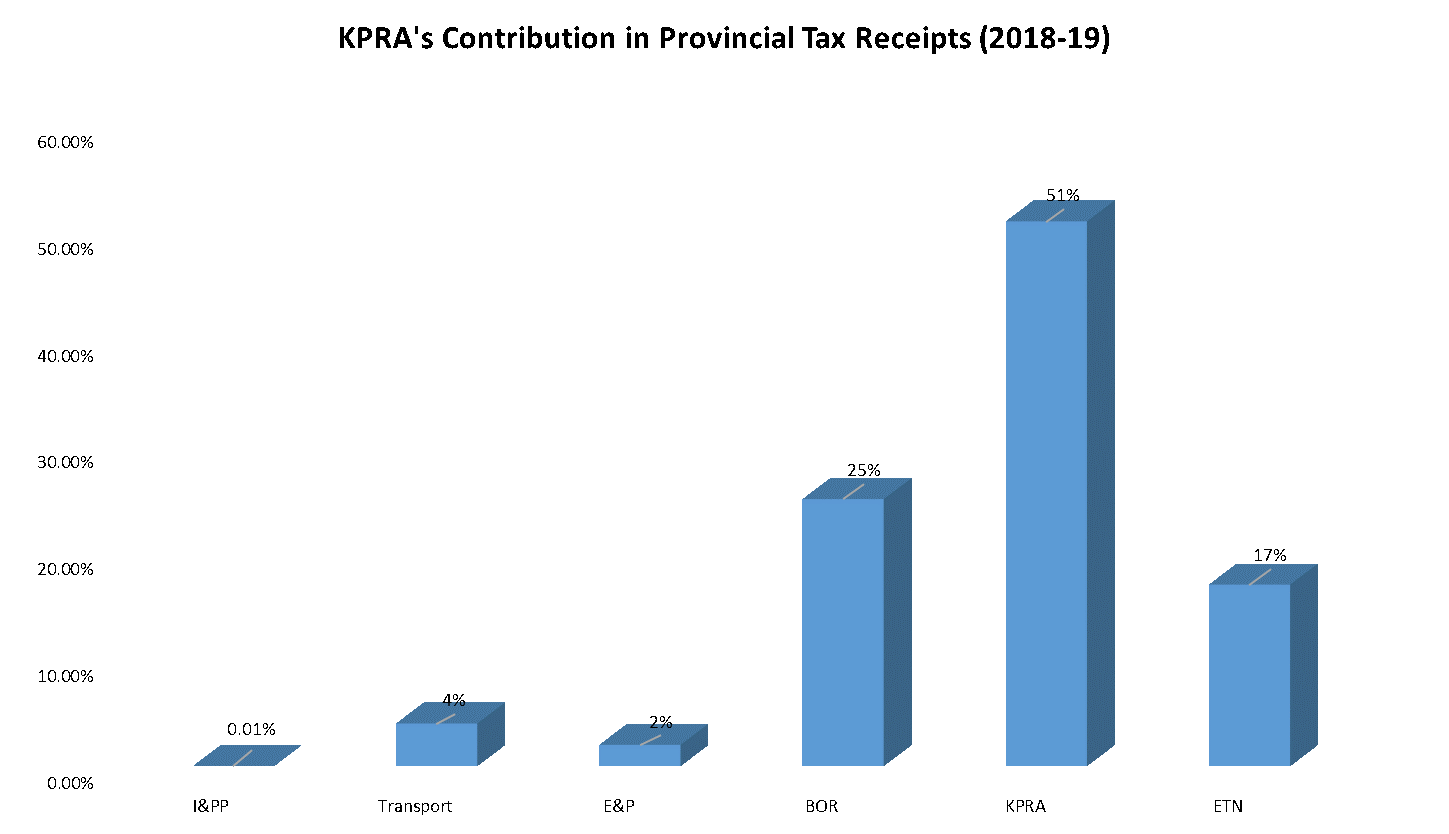

It is important to note that despite capacity issues and the COVID-19 crisis, KPRA was able to increase tax collection by 73% and generate PKR 18 billion in total sales tax revenue in 2019-20. Moreover, KPRA was also the largest contributor to provincial tax receipts in KP in 2018-19, as shown in the figure below.

Figure: KPRA’s Contribution in Provincial Tax Receipts

Source: KPRA

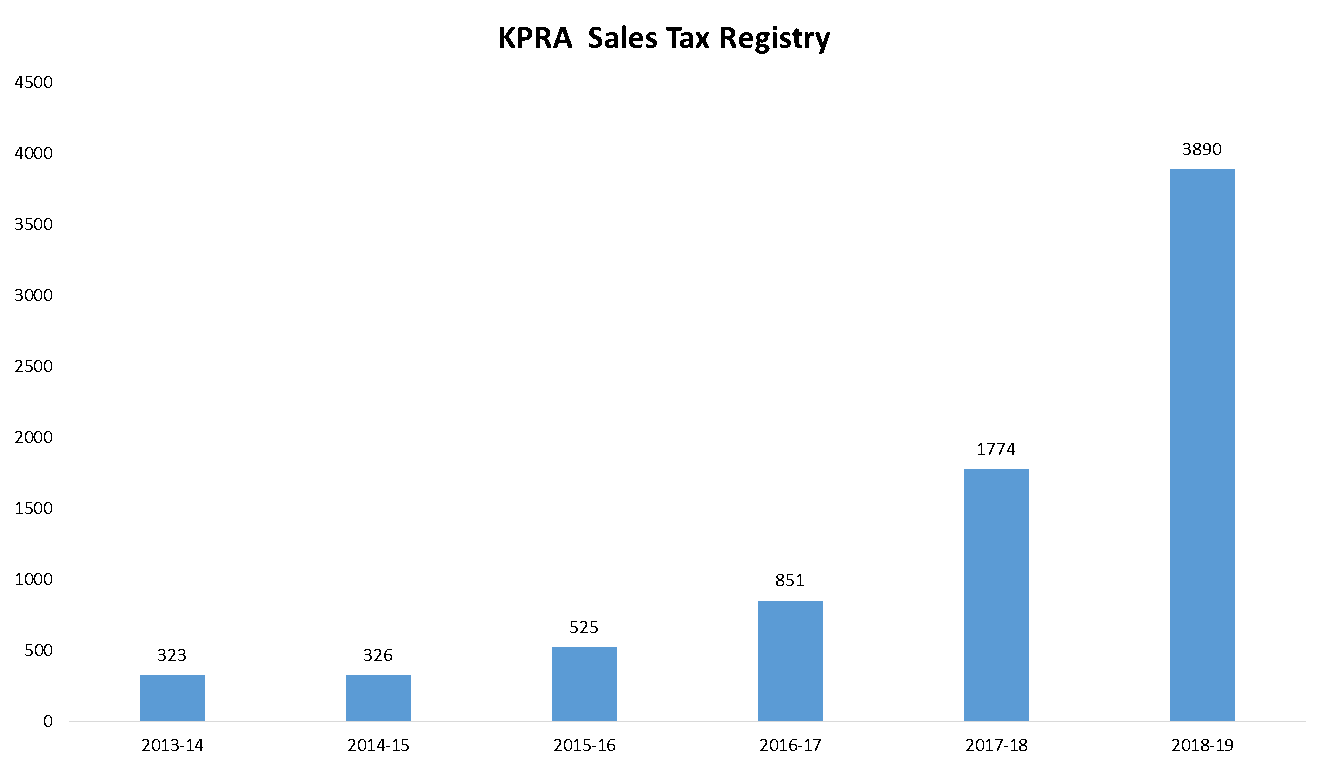

In addition to this, sales tax registrations by KPRA have also increased many fold due to inclusion of new services in the tax net, usage of readily available third party data, and departmental efforts to identify and register new taxable businesses. The figure below depicts the increase in KPRA’s sales tax registry over the past few years.

Figure: KPRA’s Contribution in Provincial Tax Receipts

Source: KPRA

Source: KPRA

Moreover, KPRA has also initiated the use of data in a scientific manner to track geographical and sectorial expansions, and identify pockets of revenue stuck in the system. It also conducts monthly performance reviews and customer satisfaction surveys to understand issues of rent seeking, and duplication of taxation between the provincial and federal governments.

Although, there is a need to expand the tax base to other potential revenue generating sectors, the provincial governments are also cognizant of the fact that the private sector needs space to grow, especially during the COVID-19 crisis. Hence, the KP government in its recent budget has reduced sales tax on services for 27 service categories to help sustain them.

The recent KP budget of 2020-21 has been deemed largely a tax-free budget, with no new tax imposed or rate of tax increased. The new budget has also provided exemptions to hotels on KPRA’s active taxpayers list from hotel tax under Excise & Taxation Department, and also exempted professionals on KPRA’s active taxpayers list from professional taxes.

Tax Reform Challenges

Despite efforts to reform the sales tax on services regime, the federal and provincial governments have encountered several challenges in both tax policy design and implementation.

i) Lack of Harmonization of Sales Tax

There is lack of harmonization of sales tax between the federal and provincial governments in Pakistan, as identified by KPRA and Punjab Revenue Authority (PRA). This has led to production inefficiencies due to denial of input tax adjustments, higher compliance costs for businesses/taxpayers which have to file for multiple tax returns, and adverse effects on Pakistan’s ranking on World Bank’s ‘Cost of Doing Business’ index. Hence, there is an urgent need to create a platform to help develop consensus among revenue collection agencies i.e. FBR, Sindh Revenue Board (SRB), PRA, KPRA and Balochistan Revenue Authority (BRA) on different aspects of the harmonization principle of taxation, tax rates, single return and tax coverage.

ii) Limited Coverage of Services in the Tax Net

The existing Sales Tax on Services Act does not have a clear and comprehensive definition of services, and this leaves services open to interpretations by the FBR. Consequently, a tax gap is created due to limited coverage of services – the yield of sales tax on services is only equal to 0.6% of Pakistan’s GDP, although services contribute approximately 56% to its GDP. Hence, the existing system incentivizes service providers to resort to litigation and evade taxes by claiming that the services they are supplying are slightly different from the schedule of taxable services under the law.

iii) Reliance on Telecom Taxes

Traditionally, the telecom sector has had the largest share in sales tax collected from services. As this sector consists of well-structured, large corporates, it is comparatively easier to collect taxes from them. In Punjab, for instance, the generation of telecom sector revenue was around 78% to begin with, however, over the years it has been reduced to around 20-25%. This setback in services tax revenue has largely been due to the Supreme Court’s decision to suspend telecom services tax in 2018. Nevertheless, GDP growth patterns indicate that there is also potential for generating sales tax revenue from other services sectors such as transport, storage, travel, wholesale and retail.

iv) Need for Improved Documentation

In addition to increasing the sales tax base, it is also important to make much needed efforts in other areas, such as documentation and tax administration. Although, relief measures are introduced to make the regulatory environment friendlier for small businesses and increase the ease of doing business during COVID-19, businesses operating across provinces still have to undergo long and complicated procedures to file returns. Even though KP and Punjab have launched initiatives to improve documentation by decreasing tax rate to 5% for restaurants that install ‘Point of Sale Software’ and allowing the use of debit and credit cards for tax payments, respectively, it has become increasingly important to move beyond an understanding of services sales tax within provincial silos, but view it more dynamically at the national level.

Lessons from Punjab’s Experience

Punjab Revenue Authority (PRA) is a semi-autonomous organization for collecting and enforcing sales tax on services in Punjab, based on the Punjab Sales Tax on Services Act, 2012. Although PRA still relies heavily on FBR’s borrowed capacity, it has been able to achieve significant milestones with regards to sales tax on services and can offer important lessons for other revenue collecting authorities.

i) Technology Innovations

PRA has prioritized technological innovations as part of its tax reforms. It was the first to introduce a Restaurant Invoice Monitoring System (RIMS) and was also able to extend this to other sectors through the introduction of an overarching Electronic Invoice Monitoring System (E-IMS). Although, initially PRA has mainly focused on Business-to-Customers (B2C) interactions, it is now inching towards Business-to-Business (B2B) invoicing – which will be mandatory with a one-year probation period, starting from 1st July, 2020. Furthermore, in light of the COVID-19 pandemic, PRA is also moving towards contact-free mass audits from this year onwards, where the contact between tax payers and tax collectors is eliminated and the audit is completed electronically. This is complemented with an e-filing system, which has converted the entire filing process, from the registration to the filing operator, online; other revenue authorities have also followed suit.

ii) Reducing Compliance Costs

PRA is moving towards a uni-return system and currently 80% of the work on this project has been completed by Pakistan Revenue Automation (Pvt.) Ltd (PRAL). The launch of this new system will be complemented by the introduction of quarterly returns to reduce compliance costs in smaller sectors and improve overall tax collection in the province. In addition to this, PRA has also launched a pre-populated returns system through which returns will be automatically filled online on a real time basis.

Cross-country learnings from Pakistan’s provinces have allowed better understanding of sales tax on services in Pakistan, but their design and implementation need to become better aligned to the national growth agenda of increasing revenues. Although, reforms like the introduction of a negative-list based sales tax regime, whereby all services are taxable unless specifically exempted, is one way to broaden the tax base and increase revenues without increasing burden on existing taxpayers, it is also important to develop consultative forums for enhancing capacity and expertise of revenue collecting authorities in Pakistan.

[1] Although, sales tax on services is completely devolved to the provinces, the revenue collecting authorities use FBR’s computerized system with Pakistan Revenue Automation (Pvt) Ltd (PRAL) for outsourcing tax collection.

This article is based on a webinar talk organised by CDPR in partnership with SEED and IGC Pakistan. Watch the full session here.

This article also draws on research and comments by Faisal Rashid (Lead Author) and Anjum Nasim (Senior Advisor).

Watch the key takeaways in a shorter video here.