Menu

What Does this Budget Say about the State of Pakistan’s Economy?

The PTI government has presented its first federal budget of Rs 7.04 trillion in the absence of a full-time finance minister. The budget announcement also came amidst a flurry of political arrests and a recent staff-level agreement to a USD 6 billion IMF program. These developments were preceded by an overhaul of the government’s key economic decision-makers.

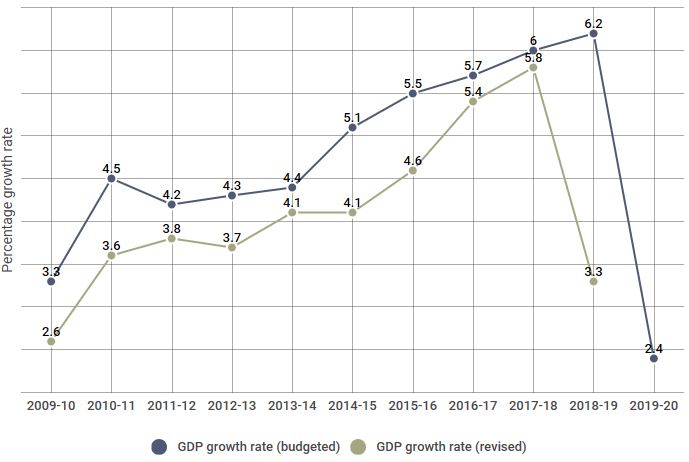

A day earlier, the latest Economic Survey released a bleak economic outlook for Pakistan. The country’s forecasted GDP growth at 3.3% – against a target of 6.2% – is set to hit a record 9-year low. Pakistan also faces the highest inflation in five years nearing double digits. Even the budget speech yesterday, was quick to acknowledge slow growth and static exports since the past five years.

Source: Dawn, June 11, 2019, Budget brief, 2009-2020

GDP growth rate for fiscal year 2018-2019 has been 3.3 percent, which is forecasted to further reduce to 2.4 percent in fiscal year 2019-2020.

Facing a looming balance of payments crisis just two years after the completion of a USD 6.6 billion IMF program, and well into another one, the government was expected to take some tough economic decisions leading up to and included in the 2020 budget. In fact, the goals unveiled for FY20 underline the scale of the economic challenges the country faces.

The budget for FY20 includes a strong commitment to narrow the primary deficit – the difference between current government spending and total current revenue (net of debt reservicing) – down to 0.6% of GDP from an anticipated 2.0% for this year.

Much of the adjustment burden falls on revenues. Not surprisingly, therefore, the budget sets ambitious targets for revenue collection combined with aggressive expenditure control. The budget is loaded with new taxes and austerity measures/spending cuts.

Is PTI on its way to fixing what ails the economy?

Pakistan’s economy can only be fixed if we address its most fundamental structural flaws. This requires an understanding of what ails the economy – a disparity between public sector spending and income, and an underdeveloped export base.

Unless policymakers take concrete measures to address the underlying causes of macroeconomic crises, this fiscal situation will repeat itself every few years.

What do we need to do to fix this?

On the one end, we need sustainable and reliable flow of income – hence an increase in revenue generation. We need tax reforms to focus on progressive taxation and reduce reliance on indirect taxation and thus protect the interests of the low-income.

On the other end, we need to rationalize expenditures, reduce losses of state-owned enterprises and streamline government machinery. At the end we need a strong export base and a strengthened business environment with a strong private sector engagement.

Does the budget reflect this commitment and offer a stabilization of the macroeconomy and its fundamentals?

The budget focuses on some aspects of the critical interventions needed to boost the economy, but there are glaring contradictions as well.

Attending to IMF conditionality, a one-time sacrifice of defence budget’s increment, more income tax slabs and higher sales taxes are temporary measures to provide breathing space to help avert a current fiscal crisis.

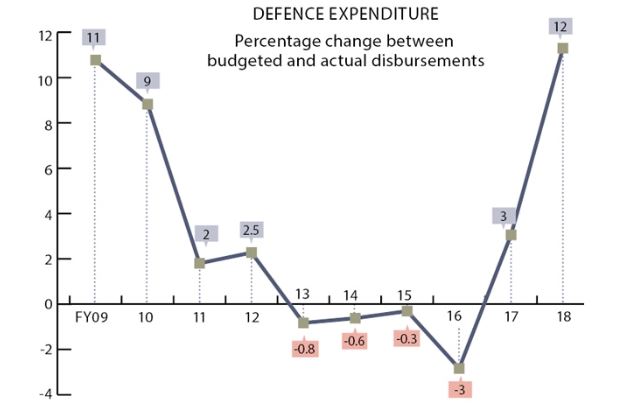

Source: Dawn, June 11, 2019

Pakistan’s armed forces have voluntarily agreed to a reduction in their budget, mainly comprising salary cuts of officer corps. In a country that continues to remain embroiled in multiple external and internal conflicts, requiring military operations against terrorist groups, this shows the resolve of military authorities to support the government.

The government is still committing to a high fiscal deficit at 7.1% compared to 7.2% of GDP in last year, owing primarily due to the large size of the debt repayments not leaving much for the private sector and businesses.

In addition, the government has announced, in a low-growth period, highly challenging revenue targets relying mostly on taxes to be collected from the masses. A plethora of new taxes have been levied and income tax slabs revised. The burden has fallen onto the salaried classes – as is typical – and is bound to hit the consumption of middle-and-low income segments to further slow down economic activity and reduce aggregate demand.

This is despite a recent World Bank report confirming that Pakistan is capturing only half of its revenue potential and needs to raise revenues by enhancing tax compliance not levying new taxes or increasing rates.

A new structure of indirect taxes is bound to increase the prices of essential items such as electricity, gas, edible oil and sugar, and will impact the overall cost of doing business and cause further inflation.

This is expected to worsen with a falling rupee which has already depreciated by more than 30% against the dollar since December 2017.

Moreover, how are exports expected to grow with a withdrawal of zero-rating facility accorded to the five leading export sectors namely: textile, carpets, leather, surgical and sports goods? Almost 65% of the exporting sector will now be liable to pay 17% duties.

In the short run, these budget commitments may become unsustainable, necessitating interim finance bills to provide quick fixes.

The PTI government has already passed two mini-budgets in the past fiscal year. Another one will only confirm the fears of the government’s worse critics.

How different is this budget from the previous ones?

Unlike the previous budgets this budget comes at the backdrop of an imminent sign off to a three-year extended fund facility with the IMF. What this means is that this budget is front loaded with prior actions to meet the IMF conditionality grounded in market-led reforms.

Imran Khan came to power promising to create 10 million jobs and build 5 million low-cost housing units over a five-year period, as part of his vision for an ‘Islamic welfare state’.

In the backdrop of a stabilization package, constraints of the IMF conditionality are expected to cut across Imran Khan’s attempts to establish a welfare state. And the new budget is underpinned by this underlying economic reality.

The total budget outlay is 30% higher than previous year. However, the focus is on two critical two critical aspects – raising revenue and cutting down expenditures. Both actions are geared towards reducing the primary deficit in the immediate future.

What stands out in this budget is the excessive focus on revenue generation, setting seemingly unrealistic, through probable, targets and austerity measures across all sectors. Tax collection targets of Federal Board of Revenue (FBR) alone are estimated at Rs 5.555 trillion to bring tax-to-GDP ratio to 12.6%. Overall federal revenues are estimated at Rs6.717 trillion – 19% higher than the previous year’s revenue.

What remains unchanged, despite the high revenue targets, is that the salaried class as always bears the brunt of the tax reforms. At the same time a rise in indirect taxes will make everyday use commodities more expensive.

However, some of the suggested tax measures are seen as positive steps towards documenting the economy. These include the condition that property cannot be registered in the name of non-filers and much higher tax rates for unregistered companies.

This budget is also focused on austerity measures and spending cuts.

The army has also decided in an unprecedented move to voluntarily skip this year’s increment. The budget outlay for defence remains unchanged at Rs 1.1 trillion. This reveals clearly government’s keenness to ensure IMF has everything it needs for a sign off.

Government’s running expenses have also been slashed down. Cabinet members will take a 10% cut in their salaries while grade 20 and 21 officers will also forgo any increment in their salaries.

The government has however taken some measures to safeguard the unprotected and low-income strata.

Some projections suggest that, over a three-year adjustment period, almost 1 million jobs could be lost and some 1 million people could fall below the poverty line. Mindful of this, the IMF insisted the new budget maintains social spending at the level of previous year.

The government has formed a new ministry to eliminate poverty to launch programs for social safety and become the umbrella organization to manage the Ehsaas program.

At the same time, stipend through BISP scheme has increased from Rs5,000 to Rs5,500, with a 10% rise for pensioners while a ration card scheme is being introduced where 80,000 people will benefit via interest-free loans.

This year’s budget also sees an increase in the minimum wage from Rs 15,000 in the last two budgets to Rs 17,500.

Where can we expect the economy to be at the time of the next budget?

Any successful IMF program requires government’s commitment to policies (some painful) that are outlined in the program. Associated with a new loan will be extensive pressure to reduce aggregate demand of which the largest burden will be on the fiscal side. A limited fiscal space can hamper Khan’s efforts to substantially enhance public spending and also hit economic growth.

The last time Pakistan entered the IMF program, growth rate stood at under four percent. Projections already reveal that growth rate will fall further to 2.4% while inflation will enter double digit figures at 13%.

This poses a challenge to the new government, voted in with high expectations to set up an Islamic welfare state. Its electorate will expect initiatives for social uplift and job creation and at the same time, high growth.

What we can expect before the next budget, in the face of an economic slow-down, is higher inflation and a tighter job market as economic activity takes a hit.

Some of this inflation could be offset if income taxes were lowered, but that is not the case as Pakistan targets to grow tax revenues at the fastest pace in recent years. With less than 1% of the 208 million people filing their returns, it may be difficult to meet the ambitious revenue targets.

While a slow-down in the demand for imports will help to prevent the dollar drain and reduce the trade gap and higher taxes along with spending cuts can help reduce budget deficit, the government may save enough to spend on development projects.

But this process will take time.

It may take two years may before economic growth can bounce back and government is able to fix the larger macroeconomic problem. If not, then we could be looking at another bailout.

A shorter version of this article was first published in Dawn. It appeared in Prism here.

Hina Shaikh is the Country Economist at the International Growth Centre (IGC).