While the current government in Pakistan has taken a multi-dimensional approach and introduced some measures to eradicate poverty, along with specific COVID-19 emergency interventions, many challenges still remain. We lay out our thoughts below on whether Pakistan is on track to achieving SDG1 by 2030, given that another 10 million are expected to move into poverty due to the pandemic.

Over the past two decades, Pakistan has made significant progress in fighting poverty, reducing it by more than half since 2000. As one of the first countries in the world to declare Sustainable Development Goals (SDGs) as part of its national development agenda and updating the national poverty line in 2016[1], Pakistan has remained committed to improving multi-dimensional poverty measures.

Progress in the last decade

As per the latest official figures, the poverty headcount ratio declined from 29.5% in 2013-14 to 24.3% in 2015-16. Of all 114 countries for which the World Bank measures poverty indices, Pakistan was amongst the top 15 that showed the largest annual average percentage point decline between 2000 and 2015. Despite this, by 2015, around 50 million people still lived below the national poverty line. Since then, the pace of poverty reduction has slowed down. This is partly due to the macroeconomic crisis resulting from structural economic issues and the lack and inadequate implementation of pro-poor policies.

Measuring poverty

Lack of accurate and consistent poverty estimates has been a key hindrance in formulating effective pro-poor policies in Pakistan. The use of monetary poverty lines tied to currency conversion rates with differing purchasing power parities, along with the use of different methodologies has led to inconsistent measures. For instance, between 2010 and 2015, show a decline in poverty headcount while an independent policy think tank estimated that around 38% of the population was still living below the poverty line in 2015; which in absolute terms meant an additional 13 million people falling into poverty. Bureaucratic and political delays in regularly updating the National Socio-Economic Registry (NSER) survey has also led to issues in targeting (the last round of the NSER survey was carried out in 2010-11).

In 2016, the government tailored a widely used global poverty measure, the Multi-Dimensional Poverty Index (MPI), for Pakistan. The aim was to capture the three main deprivation indicators: education, health, and living standards. Based on 2017-18 estimates, 38.3% of the population was deprived in at least one of the three indicators – an improvement from previous years, largely from progress in sanitation and child mortality. However, deprivation resulting from a lack of access to electricity increased.

COVID-19 and increased vulnerabilities

Vulnerabilities play a central role in perpetuating poverty as poor households lack necessary human, financial, and physical capital to withstand the negative impacts of sudden shocks. It is no surprise that COVID-19 is expected to be up to 10 times more deadly for the poor. A recent UNDP study of 70 countries, including Pakistan, estimated that COVID-19 may set poverty levels back by 9 years, with an additional 490 million people falling into multidimensional poverty.

Prior to COVID-19, Pakistan’s economy was already struggling with a fiscal crisis and undergoing an IMF-sponsored macroeconomic stabilisation programme. With one of the lowest human development indicators around, the government estimates that 56.6% of the population has now become socio-economically vulnerable due to COVID-19. As one of the youngest countries in the world, with nearly two-thirds of the population under the age of 30, a consistent GDP growth rate of 7% is required to absorb the young workforce. With a projected growth rate of only 2% post-pandemic, unemployment rates may rise drastically, perpetuating the cycle of poverty.

Despite a declining poverty rate over the past few years, the IMF has also projected a sharp reversal ahead, which may push almost 40% of Pakistanis below the national poverty line. The cost of the expected economic slowdown due to COVID-19 containment measures, invariably relying on some form of lockdown, will mostly be borne by the estimated 24.89 million daily wage earners, piece-rate workers, and self-employed in. These groups are more vulnerable to pandemic-induced poverty due to a lack of access to social protection programmes.

What didn’t work in the past?

Pakistan has a long history of poverty reduction policies and interventions. However, the persistently high poverty levels reflect the inadequacy of these measures resulting mainly from a focus on static measures and limited outreach. Poverty reduction programmes account for just about 2% of GDP; due to lack of coordination, inefficient implementation, and inadequate monitoring and evaluation, there is often duplication and fragmentation across these programmes.

Despite deep-rooted economic inequalities and the sheer number of people impacted, policymakers have largely steered clear of addressing the issue of inequality. It is estimated that 40% of all children born in abject poverty will remain in the lowest income quintile, another 40% will improve slightly from very poor to poor, while only 10% will be able to transition out during their lifetime[2]. Research also shows that while relatively high economic growth in 2001-04 was not pro-poor, the low growth period of 2005-10 saw better poverty indices. This indicates that policy interventions for the poor are not all the same; there is a need to have a more targeted approach for transitionary and inter-generational chronic poor.

What Pakistan has done right?

Early indications point to the government’s commitment to poverty reduction, as it has pledged to reduce poverty by 6 percentage points to 19% by 2023. Measures include increasing poverty alleviation expenditures and ensuring that vulnerable groups such as women, children, and people with disabilities receive needed aid.

One such measure is the integration of more than 134 fragmented and insufficiently managed social protection programmes, and prone to political manipulation, under ‘Ehsaas’. This is a new overarching programme launched in 2019, built on the framework developed under the Benazir Income Support Programme (BISP). BISP is one of South Asia’s largest cash transfer programmes and Pakistan’s flagship social protection initiative. Launched in 2008, BISP currently caters to 5.7 million ultra-poor families via unconditional cash transfers to women.

In response to COVID-19, the government quickly implemented the Ehsaas Emergency Programme, under which low-income households gained access to financial assistance through text messages. In the first phase of this programme, 12 million families were provided with a monthly stipend of 12,000 PKR ($72). More recently, the programme has been extended to include 17 million families, around half of the total population of Pakistan.

The government has also made efforts to de-politicise poverty measures. There is great optimism that under the current government, the NSER survey, which will cover at least 27 million households, will be completed by 2021 and enable smart poverty targeting.

Is Pakistan still on track to achieve SDG1?

Even before the pandemic, Pakistan was categorised as being ‘off track’ to halve multidimensional poverty by 2030, and less likely to achieve SDG1 with current interventions. This has largely been due to inadequate policy responses from successive governments, despite some good progress on poverty alleviation in the early 2000s. The current government, however, has taken some steps in the right direction. While there is growing consensus on the benefits of a rapid policy response, there has historically been a lack of focus on more long-term sustainable efforts.

There is increasing evidence, across South Asia, that an ‘income-mediated’ approach to SDG1 will have limited success and more ‘expenditure led’ policies are required. Looking ahead, well-informed income and poverty projections can provide a blueprint for more proactive, targeted and sustainable policies, with a focus on alleviating extreme poverty.

[1] Research by Lahore University of Management Sciences (LUMS) in collaboration with Oxfam.

[2] Instead of using the Food Energy Intake (FEI) approach, a Cost of Basic Needs (CBN) approach is now employed

This blog has originally been published on the International Growth Centre (IGC) website here.

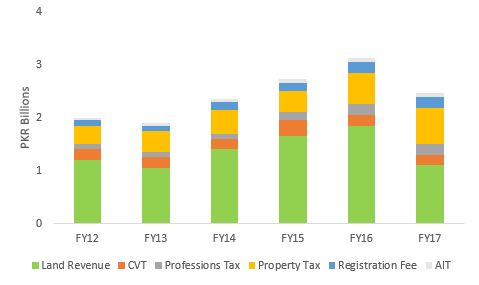

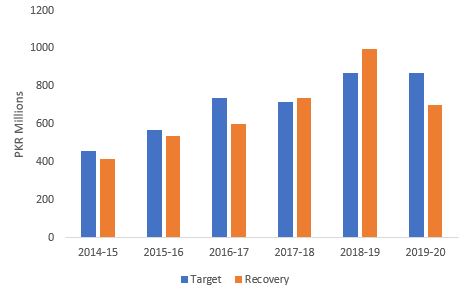

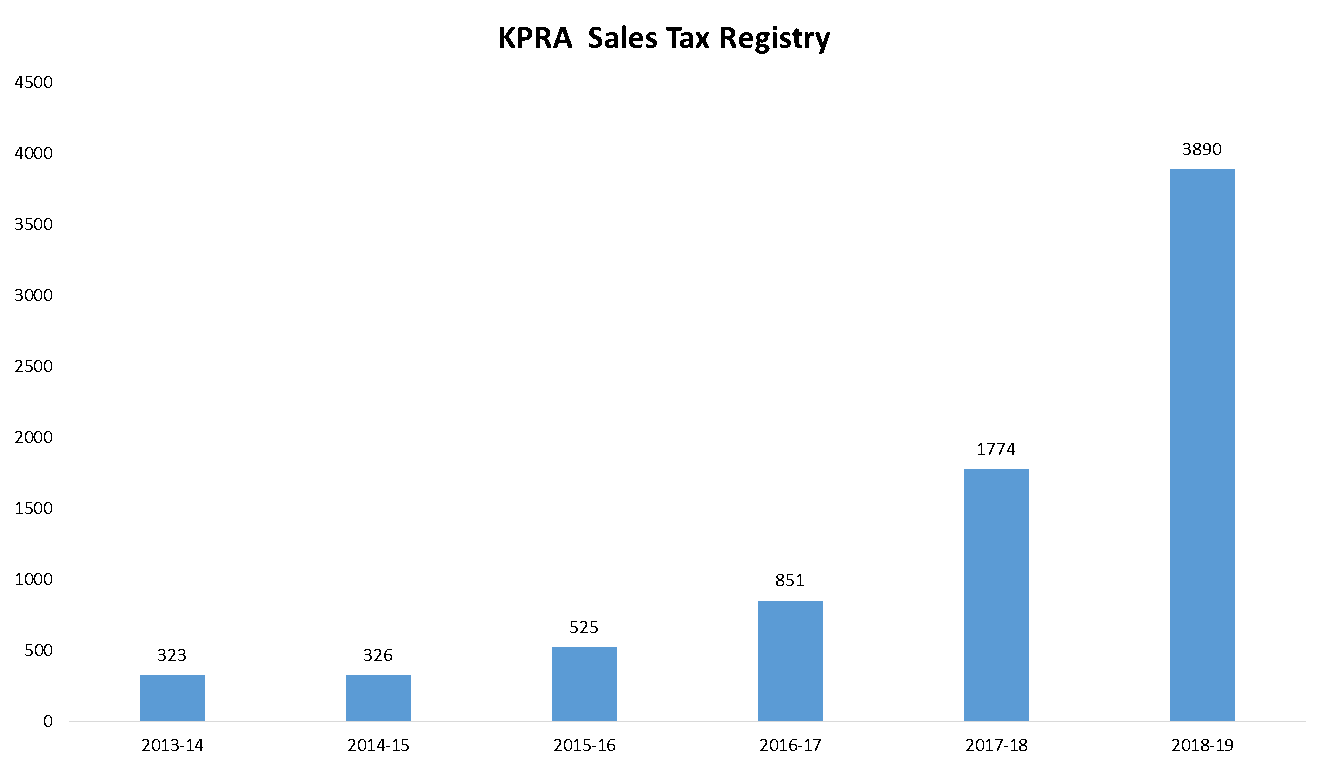

Source: KPRA

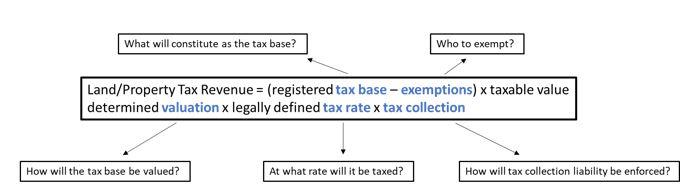

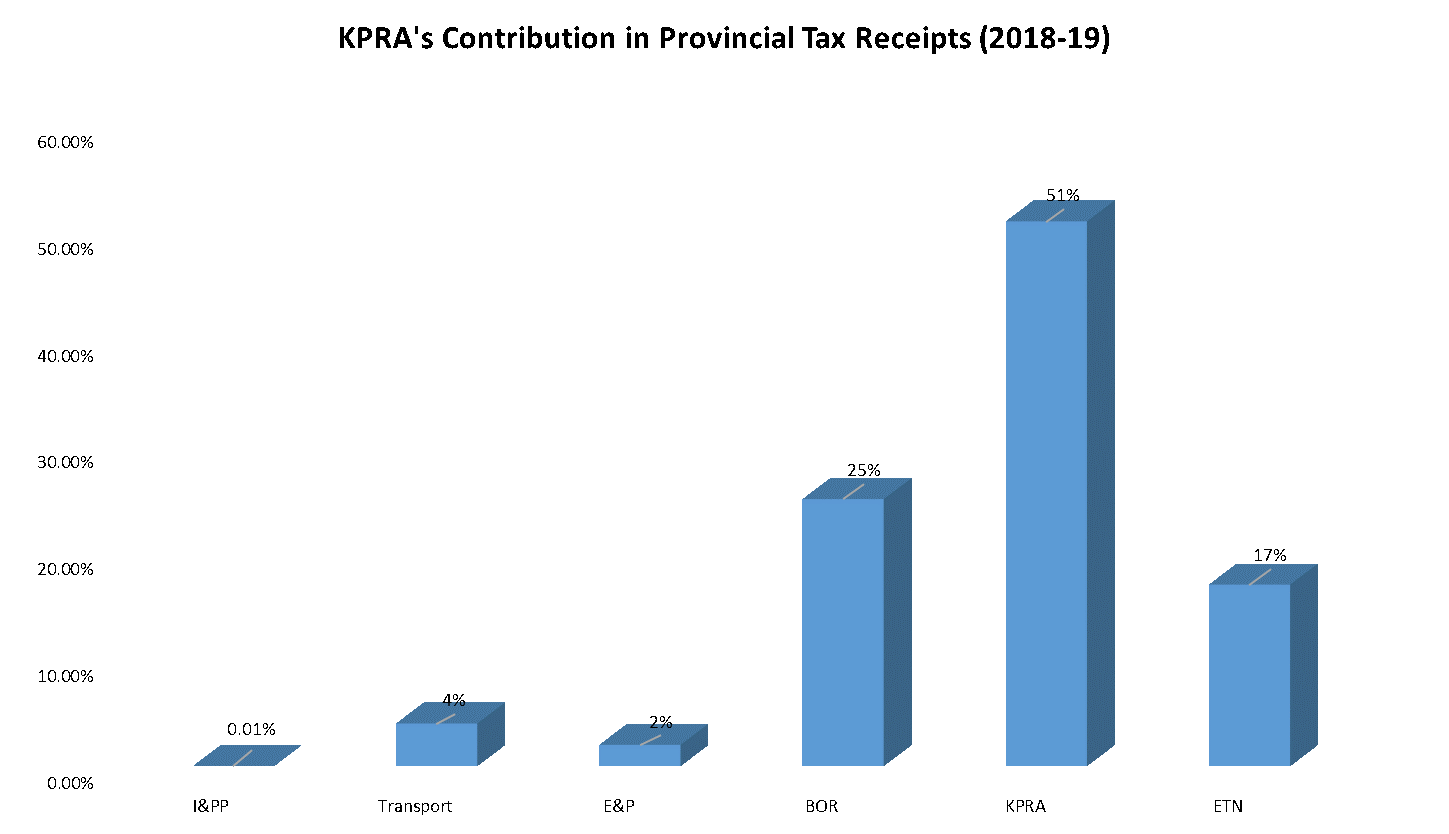

Source: KPRA