Menu

Engaging with Pakistan’s exporting firms to improve trade prospects

By Salamat Ali and Ghazan Jamal

Pakistan’s struggle to improve its exports is no secret, nor is the growing pressure on the government to stem this downward trend. In 2015-16, according to the Trade Development Authority of Pakistan (TDAP), the country’s exports fell by over 12 percent compared to the previous year, to a mere USD 20 billion.

Key to making export friendly policies from the government’s side is to better understand the nature of exporting firms in Pakistan. A recent study by Salamat Ali partly does that by investigating the impact of trade costs on the composition of Pakistan’s exports and the behavior of its exporting firms.

In the study, trade costs are defined as the cost associated with transporting the product from the factory to its destination. That includes freight charges, border costs both at Pakistan and the destination market, and other customs-related surcharges. The study examines the World Bank’s trade cost dataset, exporter dynamics dataset (EDD), FBR’s national data sources, Centre d’Etudes Prospectives et d’Informations Internationales (CEPII), and other open data sources collected by the World Bank and UN Conference on Trade and Development (UNCTAD).

The study has four key findings: First, exporting is a rare activity in Pakistan. Only 23 percent of all firms in Pakistan export their products.

Second, due to the high cost of exporting and a lack of competition in the domestic market, on average, even exporting firms sell 70 percent of their output domestically.

Third, among exporting firms only a few export multiple products to multiple markets. In fact, most exporting firms concentrate on the same few markets with the same products.

And finally, the survival rate of Pakistani exporting firms is very low. Many firms and products exit the exporting market after a few years. This is especially true of exporting firms that are based in relatively remote areas from seaports.

It would not surprise anyone that the data shows that as trade costs increase, exports go down. This is shown in the graph below, where Pakistan’s bilateral trade costs and exports to the destination country are plotted:

Figure 1: The relationship between exports and trade costs

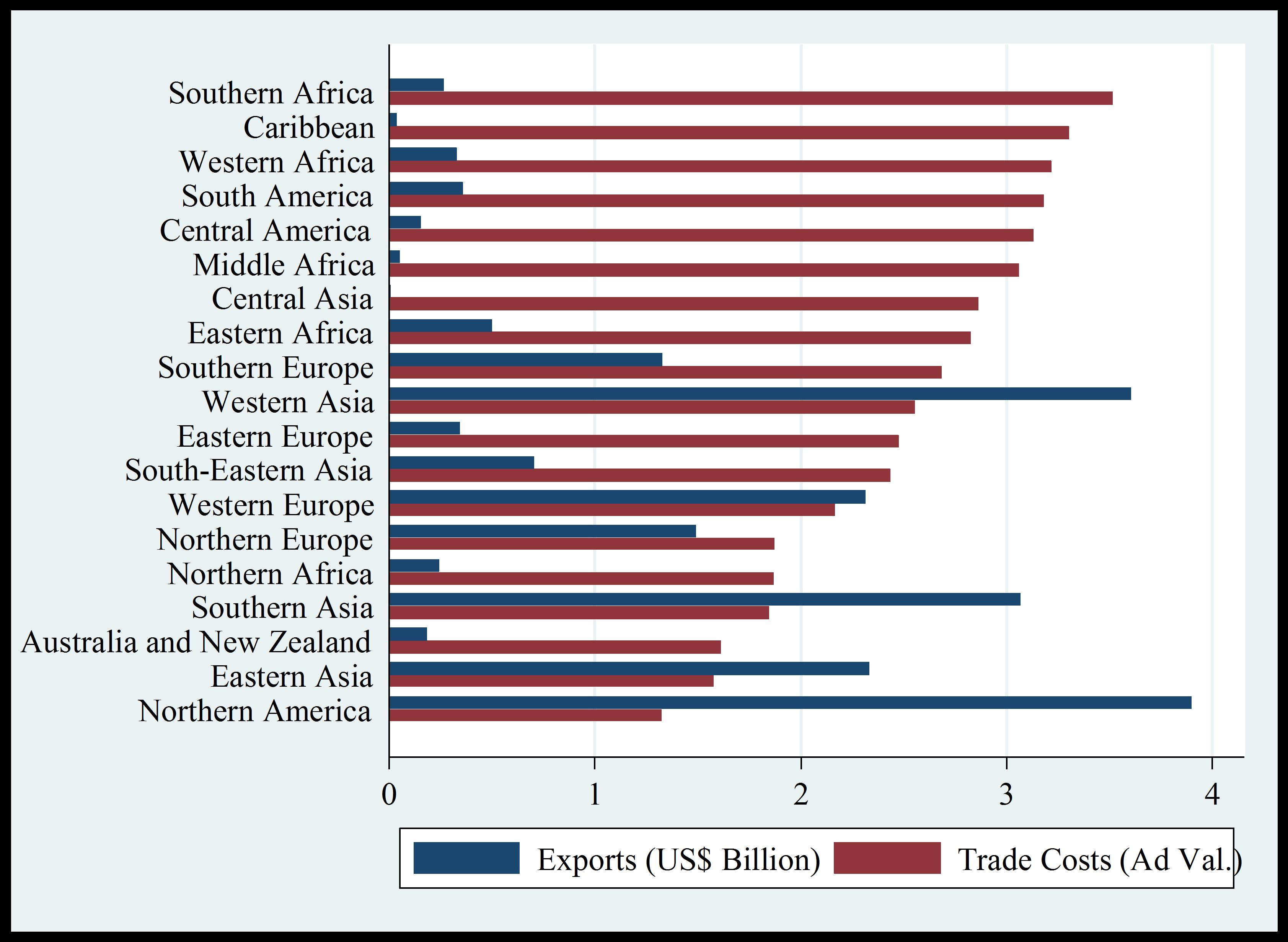

A regional breakdown of the same as represented in Figure 2, which shows that Pakistan’s trade costs are lowest with Northern America and Eastern Asia, and these correspond to two major destinations for Pakistani exports as well. On the other hand, Pakistan’s trade costs are highest with Southern Africa and the Caribbean and these correspond to some of the lowest export destination for Pakistani products.

Figure 2: Pakistan’s exports and trade costs by region

Contrary to popular belief, in 2015, Pakistan’s border-related costs associated with exporting and importing a 20ft container was much lower than some other countries in the region like India and Bangladesh. This shows that our customs and port operations are more efficient than these countries. The comparison can be seen in the table below.

Table 1: Pakistan and comparator countries’ border-related costs of exporting and importing

| Parameters | Pakistan | Bangladesh | India | China | Singapore |

| Cost of Exporting a 20ft Container | 765 | 1,281 | 1,332 | 823 | 460 |

| Cost of Importing a 20ft Container | 1,005 | 1,515 | 1,462 | 800 | 440 |

| No. of Export Documents | 8 | 6 | 7 | 8 | 3 |

| No. of Import Documents | 8 | 9 | 10 | 5 | 3 |

However, our bilateral trade costs are comparatively much higher, putting our exporting firms at a disadvantage. The table below shows these figures for Pakistan comparing to other countries in the region:

Table 2: Bilateral trade for Pakistan, India, China, and the world

| Year | World | Pakistan | India | China |

| 2003 | 242 | 223 | 229 | 192 |

| 2004 | 236 | 211 | 213 | 177 |

| 2005 | 234 | 214 | 209 | 171 |

| 2006 | 232 | 216 | 201 | 168 |

| 2007 | 228 | 221 | 198 | 166 |

| 2008 | 230 | 233 | 194 | 166 |

| 2009 | 231 | 235 | 191 | 164 |

| 2010 | 222 | 224 | 183 | 153 |

| Average | 232 | 222 | 202 | 170 |

Source: Bilateral trade costs dataset, the UN-ESCAP

The concerning trend for Pakistan in this period is that as there is a clear downward trend in bilateral trade costs globally as well as in the cases of India and China. However, in the case of Pakistan trading costs have fluctuated without much improvement. This shows inconsistency of policy and the lack of a concerted effort to improve our export regime. These high costs mainly pertain to relatively large input tariffs on imports of intermediate inputs used for manufacturing for exports, poor transport network to connect manufacturing regions in the North with seaports in the South and high costs of other inputs such as electricity and natural gas.

The study lays out some very tangible steps that the government can take to bolster the country’s exports both in the immediate and longer terms. These are summarized as follows:

Engage more actively with larger exporting firms. The top one percent of firms take up 50 percent of all exports, while the top five percent of firms mediate over 75 percent of all exports. The top one percent comprise not more than 100 firms, and engaging with them to support their exporting activities can generate immediate results. This was the approach taken by South Korea at the time when it was looking to boost its exports as well.

Further liberalize the importing regime. This is because large exporters are also large importers. On average, 20 percent of imports are used to produce exports. Pakistan’s highest import tariff on inputs puts exporting firms at a great disadvantage globally. Moreover, the reduction in import tariff will increase competition in the domestic market and push inward-focused firms to explore international markets.

Make better use of new trade policy tools and explore potential trading partners. There are about 700 active free trade agreements (FTAs) globally and on average every country has 10 FTAs. However, Pakistan is only party to 5 FTAs namely with China, Malaysia, Iran, Indonesia, and Sri Lanka, and these countries also correspond to some of Pakistan’s main export destinations.

Improve trade-processing infrastructure. This is especially true for landlocked parts of Pakistan. As was observed earlier, the survival rate in the international market is particularly low for exporting firms operating out of relatively remote parts of Pakistan.

Salamat Ali is a senior trade associate at The Commonwealth’s Trade Division and an applied trade economist at the University of Nottingham.

Ghazan Jamal is a Pakistan country economist at the International Growth Centre.